The Inland Revenue Department’s head office looks less than distinguished. Externally, the building ranks between ugly and dreary. Internally, it is crowded and poky. The architecture seems to reflect the experiences of the taxpayers who have business there.

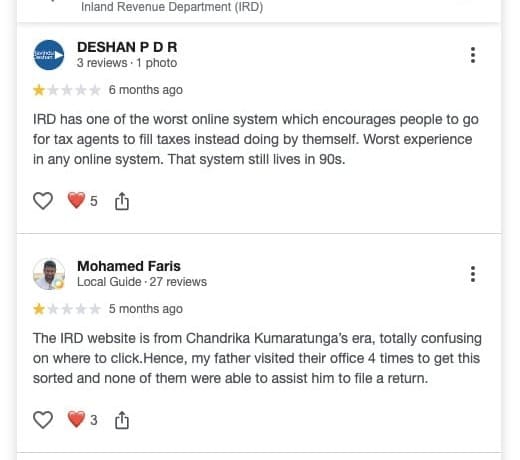

Their descriptions of the department are unflattering. Here are some reviews from Google Maps. “Visit this place and you’ll know exactly why Sri Lanka isn’t getting any foreign investments, why people hate starting business, and why the country’s economy sucks,” explains one irate taxpayer. Another called it “one of the weakest departments in Sri Lanka”, concluding that “nothing good can be said about the IRD”.

But change, real change, is in the air. The government recently promised to build the department a new HQ. Not entirely coincidentally, the IRD itself has recently begun to look more lively and pro-active. It’s beginning to develop the capacities, practices, and attitudes that one would expect of a revenue agency in a relatively high income democracy with an open, globalised economy.

And it could not be more timely. Last year, I suggested that, in its technology and practices, the IRD was about two decades behind many African tax agencies. That remains broadly true, but there is now a sense of movement, mostly in the right direction.

Paralysed by paperwork

It’s unlikely that most taxpayers have yet experienced anything that would justify this optimism. Their perceptions are still shaped by the fact that the IRD continues to use outdated and inefficient processes and technology. It has also long been poorly resourced, especially in personnel terms.

The IRD still organises its work in ways that would gladden the heart of the most punctilious 20th century government filing clerk. Files are dealt with in exactly the same order in which they were received, regardless of tax value. Not only should all figures in tax returns reconcile exactly, but all supporting documentation must be 100% formally correct.

The organisation is yet to embrace the practice of risk analysis that is central to modern tax administration: identifying which taxpayers and transactions pose the highest risk of non-compliance, so that limited staff and audit resources can be targeted where they will have the greatest impact.

Many of the department’s routine operations remain paper based. This is inefficient and generates higher error rates. It particularly becomes a problem when the organisation continues to insist that all the numbers in tax returns should reconcile precisely — and in consequence spend a lot of time trying to sort out ‘errors’ that may amount only to a few hundred rupees.

The functionality of the digital tax administration platform, RAMIS, that was installed a decade ago, has expanded only slowly. It was only from June 2025 that taxpayers were required to submit their tax returns online. One cause is the acute shortage of competent IT staff. Public sector salaries and government recruitment practices seem to offer no way out. RAMIS doesn’t function outside office hours.

The effects are apparent. There is — and has long been — a large backlog of historic tax arrears that are formally subject to legal dispute. At the end of 2024, these arrears amounted to 44% of the total revenue collected by the IRD in that year. Many of them will never be recovered.

This was made worse due to the completely misconceived 2023 government policy of requiring all adults to register with the IRD — when only about 3% of the population were registered. The tax payer register is now bloated with the details of a large number of people who should not be there: they are highly unlikely ever to be liable for direct taxes like income tax or withholding tax.

The IRD office has been choked with people confused about these registration rules, or anxious because they have received completely unexpected, and unnecessary, demands that they should file tax returns at short notice. Those who are unlikely to actually pay tax need to be removed. They likely number at least half a million people.

Meanwhile, other tax payers need a lot more attention. The department’s large taxpayer unit, which in most tax administrations is a major collector of revenue, is very much behind on auditing large taxpayers. Its staff are tied up in court cases stemming from appeals made against previous assessments.

Neglected and ignored

These are mostly longstanding problems, and in most respects not the fault of the IRD staff or management. Since around 1990, successive finance ministers and treasury secretaries have mostly neglected and ignored the IRD. The department’s managers have long complained that they haven’t been consulted on tax policy changes that affect their work.

Requests for resources, especially replacements for retired staff, have been ignored. The fact that technology and working methods have fallen increasingly behind international norms has attracted little attention. In January this year, a hundred newly-recruited Inland Revenue Service officers began work. That’s a 10% increase. Prior to that, the last major staff recruitment was two decades ago.

Until this latest recruitment, very few staff members were from the age groups that had grown up in a digital environment. At the end of 2024, less than 3% of the Inland Revenue Service officers were aged below 30 years.

New recruitment and the promise of a new head office reflect the fact that the current government has reversed the long established neglect of the IRD. Since 2023, Sri Lankan governments have had no choice but to radically increase public revenue. Some large increases in tax rates dealt with the immediate problem. Attention has turned to improving the underlying revenue machinery.

SVAT success

The most tangible reform relates to the abolition, from January, of the Special VAT system that effectively exempted exporters from paying VAT. The consequences were widely feared. It was reasonably expected that exporters would face massive challenges in obtaining VAT refunds from the IRD, and in consequence would be vulnerable to major cash flow problems. So far, the refund process has worked almost seamlessly.

A major reason is that a large export company cooperated with the IRD in successful experiments to use an API to link its own digital system to RAMIS for the purposes of dealing with VAT refunds. This kind of cooperation with the private sector is good but far from the norm.

Over the last two years, the department, step by step, is finding its mojo. The government has made tax reform a priority. The president’s office has created a bureau for revenue administration reform and modernisation, and the Treasury, a tax policy analysis unit.

These efforts are beginning to bear fruit. The IRD and Customs are starting to cooperate for the first time, signing an agreement on joint-investigations. Previously, the two agencies worked completely independently of each other. An inter-agency tax crime unit has also been established.

These initiatives seem bureaucratic, and remote from taxpayers’ concerns. The reforms are, however, significant for an organisation that has long been neglected, and hermit-like in its lack of engagement with other parts of government.

They certainly mean a great deal more than a simple reversal of the historic decline. If this continues, the department’s Google reviews could look quite different in a few years.

Comments ()